Assets acquired by companies change in value throughout their useful lifecycle and require periodic reevaluation to establish current value, so that financial statements will represent an accurate picture. These periodic evaluations apply to all company assets: tangible assets such as buildings and inventory and intangible assets such as customer relationships, contracts and goodwill.

An impairment test for goodwill is a means of assessing the current value of goodwill. Goodwill impairment testing was, until recently, a complex and expensive process, which relied on valuing everything else to establish the “leftover” value that could be attributed to goodwill. New guidelines for goodwill impairment testing have greatly simplified this process.

In this article, we’ll examine goodwill and compare the previous and current methods for impairment testing.

What exactly is “goodwill?”

Goodwill is an intangible asset that only arises from an acquisition, when a purchaser pays a price higher than the collective tangible and measurable intangible assets to acquire a business. The excess of the purchase price not assigned to these assets constitutes the goodwill value. As an intangible asset, goodwill is listed with the long-term assets on the purchaser’s balance sheet.

Because the value of goodwill is subjective, accounting standards require that it be tested for impairment on a regular basis, and written down if impairment occurs. (Tweet this!)

Need to get a handle on the current value of your goodwill assets? Consult with us on a free discovery call.

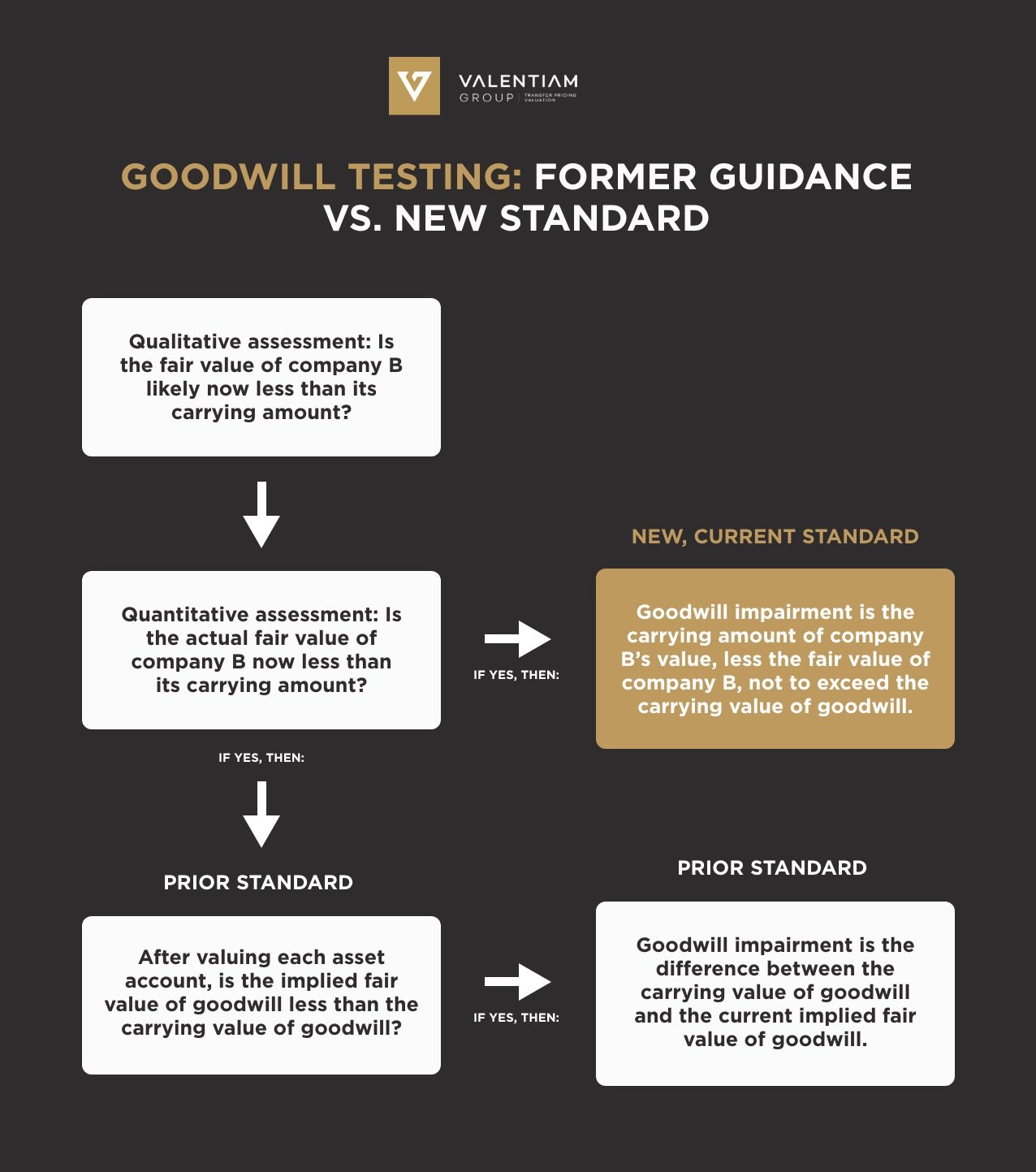

New Goodwill Impairment Test Eliminates Quantitative Assessment

The new standard for measuring goodwill impairment compares the actual fair value of measurable assets against the total carried value of the acquired company, and assumes that any difference between the two represents only the amount of goodwill impairment. This difference is then reflected on the balance sheet as a reduction in the company’s long-term assets.

Goodwill impairment example:Under the new guidance, if the overall value of company B is less now than it was at the time of purchase by company A, that reduction in value is assumed to be due to goodwill impairment only, not to exceed the carrying value of goodwill. For example, if company A purchased company B for $100,000, and company B’s measurable assets at the time of the sale were $95,000, the carrying value of goodwill is $5,000. If a year later, the measurable assets acquired from company B are calculated at $85,000—$10,000 less than their value at the time of purchase—only $5,000 of the reduction in asset value can be attributed to goodwill impairment. |

Former Standard For Goodwill Impairment Testing Versus Current Standard

The prior standard for measuring goodwill impairment consisted of a three step process:

- Qualitative assessment: Is the fair value of company B likely now less than its carrying amount? If yes, then:

- Quantitative assessment: Is the actual fair value of company B now less than its carrying amount? If yes, then:

- Quantitative assessment: Is the implied fair value of goodwill now less than the carrying value of goodwill? If yes, then the goodwill impairment is the difference between the carrying value and the current implied fair value.

Both the former guidance for goodwill testing and the new begin with a qualitative assessment—a judgement call. If it is likely that more than 50% impairment has occurred as a result of recession, cost increases, declining cash flow, management changes, sustained decrease in share price, or other factors, then further goodwill impairment testing is required.

As seen in the flowchart above, the issue with the prior standard is that obviously, since goodwill value can only be calculated as a remainder after the value of all tangible and measurable intangible assets have been calculated, it requires a much more extensive analysis to determine. The new guidance for goodwill impairment testing eliminates the need to calculate the value of all measurable assets by assuming that the change in fair value of a company’s assets is all due to the change in goodwill.

The downside of the new approach is that the valuation of goodwill is now much less precise, because it isn’t being directly measured; it is being valued indirectly by assuming that the entire value change of the acquired company flows solely to goodwill. While the new approach is much less costly and complex, this lack of precision can have an impact on the valuation of equity, as well as tax consequences that you should discuss with your valuation and tax advisors.

Need assistance in calculating the value of your assets—including goodwill?

Valentiam can help. Our industry experts are trusted by some of the world’s largest and most complex organizations to assist in establishing values for accounting and tax purposes. Give us a call to explore how we can assist you in all of your valuation needs.

Topics: Goodwill impairment test